Auto insurance is a necessary expense, but for many drivers, it feels like a never-ending financial burden. Premiums seem to rise every year, even when nothing changes—no accidents, no tickets, no new car. This leaves many people asking the same question: Why am I paying more, and what can I do about it?

The truth is, auto insurance pricing is not random. Insurance companies use complex formulas, risk models, and behavioral data to determine how much you pay. While this may sound intimidating, it also means there are clear and practical ways to reduce your costs—if you know where to look.

This article outlines seven easy, proven ways to slash your auto insurance costs without sacrificing the protection you need. These strategies are realistic, ethical, and effective, whether you are a daily commuter, a business professional, or someone managing a family budget.

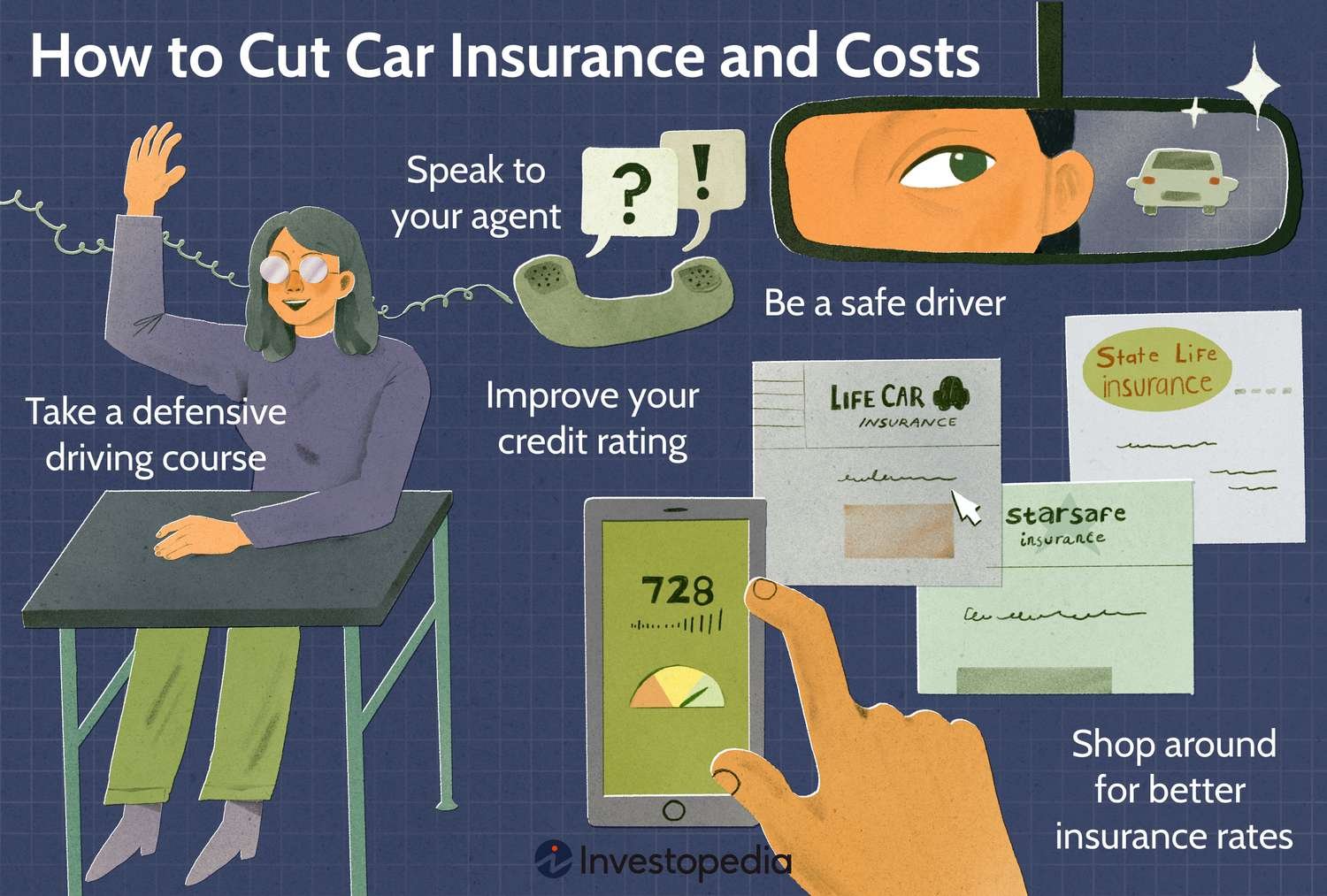

Way #1: Shop Around More Often Than You Think You Should

Loyalty Rarely Pays in Auto Insurance

Many drivers stay with the same insurance company for years, believing loyalty will earn them better rates. Unfortunately, auto insurers often reserve their best pricing for new customers, not long-term ones.

Over time, your premium may quietly increase due to:

- Company-wide rate adjustments

- Regional risk changes

- Inflation and rising repair costs

Why Comparing Quotes Works

Different insurers weigh risk differently. One company may heavily penalize age, while another prioritizes driving history or vehicle type. As a result, the same driver can receive vastly different quotes.

How to Shop Smart

- Compare quotes at least once per year

- Use both online tools and direct insurer quotes

- Include regional and lesser-known insurers

- Ensure coverage levels are identical for fair comparison

Bottom Line

Even if you love your current insurer, comparison shopping is one of the fastest ways to slash costs.

Way #2: Raise Your Deductible Without Raising Your Risk

Understanding Deductibles

Your deductible is the amount you pay before insurance covers the rest. A lower deductible means higher premiums, and a higher deductible means lower premiums.

The Smart Adjustment

Many drivers choose low deductibles by default, without considering:

- Their savings

- Claim frequency

- Long-term cost

Raising your deductible from $250 to $500 or $1,000 can significantly reduce your premium—often by 10–30%.

Risk vs Reward

If you:

- Have emergency savings

- Rarely file claims

- Drive responsibly

Then a higher deductible is usually a smart move.

Bottom Line

A carefully chosen deductible can slash premiums without increasing real-world risk.

Way #3: Eliminate Coverage You No Longer Need

When Less Coverage Makes Sense

As your car ages, certain coverages become less valuable—especially collision and comprehensive insurance.

If your car is worth only a few thousand dollars, paying high premiums to protect it may not be cost-effective.

Questions to Ask Yourself

- What is my car’s current market value?

- How much am I paying annually for extra coverage?

- Could I afford to replace the car if necessary?

Example

Paying $900 per year for collision coverage on a car worth $3,000 rarely makes financial sense.

Bottom Line

Match your coverage to your car’s value—not to habit.

Way #4: Unlock Discounts You Probably Didn’t Know Existed

Discounts Are Not Automatic

One of the biggest secrets in auto insurance is that many discounts are not applied unless requested.

Common hidden discounts include:

- Safe driver discounts

- Low-mileage discounts

- Defensive driving courses

- Anti-theft and safety features

- Multi-policy (bundle) discounts

Why Insurers Stay Quiet

Discounts reduce revenue. If customers don’t ask, insurers often won’t offer them.

How to Maximize Discounts

- Call your insurer and request a full discount review

- Update your driving habits and mileage

- Provide proof of safety features or completed courses

Bottom Line

Asking the right questions can instantly reduce your premium.

Way #5: Improve Your Credit Score (Yes, It Matters)

Credit and Insurance Are Connected

In many regions, insurers use credit-based insurance scores to estimate risk. Drivers with higher credit scores tend to:

- File fewer claims

- Cost insurers less money

As a result, poor credit can dramatically increase premiums—even if you’ve never had an accident.

Small Improvements, Big Savings

Raising your credit score can:

- Lower premiums

- Improve policy options

- Reduce overall financial stress

Practical Steps

- Pay bills on time

- Reduce credit card balances

- Check reports for errors

- Avoid frequent credit inquiries

Bottom Line

Better credit often equals lower insurance costs.

Way #6: Drive Less and Prove It

Mileage Matters

The more you drive, the higher your risk. Many insurers now offer discounts for:

- Low annual mileage

- Remote or hybrid workers

- Usage-based or telematics programs

Telematics Programs

These programs track driving behavior such as:

- Speed

- Braking

- Time of day driving occurs

Safe drivers can earn significant discounts.

Who Benefits Most

- Remote workers

- Retirees

- City residents with short commutes

Bottom Line

If you drive less or drive well, make sure your insurer knows it.

Way #7: Be Strategic About Filing Claims

Every Claim Has a Cost

Even small claims can lead to:

- Higher premiums

- Loss of claim-free discounts

- Increased long-term costs

When Not to File a Claim

- Repair cost is close to your deductible

- Damage is minor and cosmetic

- You have filed recent claims

Long-Term Thinking Wins

Insurance is designed for significant financial protection—not convenience.

Bottom Line

Fewer claims often mean lower premiums over time.

Bonus Tips to Cut Auto Insurance Costs Further

- Bundle auto and home or renters insurance

- Choose cars with high safety ratings

- Avoid coverage gaps at all costs

- Maintain a clean driving record

- Review your policy every year

Real-Life Example: Cutting Costs Without Cutting Coverage

Sarah, a working professional, reduced her auto insurance costs by:

- Switching insurers after comparing quotes

- Increasing her deductible

- Bundling policies

- Improving her credit score

- Avoiding unnecessary claims

Result: Over 40% savings in two years, with stronger coverage than before.

Conclusion

Auto insurance doesn’t have to drain your finances. With the right strategy, you can significantly reduce your premiums while keeping the protection you need.

The 7 Easy Ways Recap:

- Shop around regularly

- Raise deductibles wisely

- Remove unnecessary coverage

- Ask for every available discount

- Improve your credit score

- Drive less and document it

- File claims strategically

When you take control of your insurance decisions, you stop overpaying—and start saving.

Summary:

The law requires you buy auto insurance. So if you must get cover, how can you reduce costs ? Here’s 7 easy ways to get the best possible auto insurance deal.

Keywords:

Car Inurance, Car, Inusrance, Finance, Business

Article Body:

Here’s 7 easy ways to get the best possible auto insurance deal.

- Multiple Quotes

Get multiple quotes – use the internet and call a few brokers. It’s easy to gather some good comparison quotes.

Remember to get different types of quotes e.g one from a direct-sell insurance company; another from an offline broker who keeps a database of quotes; and a couple from the internet.

Cheapest might not mean best. Will they pay out if you make a claim ? How financially secure ? How reputable ? Check around with family and friends, and look for online reviews.

- Different type of car

Insurance costs vary depending on car type. Obviously, that $100k sports model costs more to insure than your average runabout. If you’re planning to buy a new car, check insurance costs before you buy. I once set my heart on a beautiful, high performance, highly tuned Pontiac.

Luckily I checked the auto insurance before I bought it, because I couldn’t get insurance. Every broker, every insurance company flat turned me down because I lived in a high car-crime area. So I had to forget the car of my dreams until I moved up-town.

- Age and Value of Car

Maybe you’re buying a used car ? Maybe your car saw better days a few years ago, and now values much lower ? So why pay for high-priced auto insurance ? In particular, do you still need fully comprehensive coverage ?

A good rule of thumb multiplies insurance premium by 10, and compares that figure with your car value. So if you’re quoted $1000 premium and your car is worth less than $10,000 you may want to think if comprehensive represents good value. If you drop collision and/or comprehensive coverage, you should get big savings.

- Higher deductibles (excess charges)

Most auto insurance companies use deductibles to keep policy cost down. Deductibles, or excess charges, show what you pay before your auto insurance policy kicks in. Try requesting quotes with different levels of deductibles, and see how your quotes vary.

Most internet quote forms contain a box where you can specify preferred level of deductibles. Ask your broker his recommended level. For example, going from $250 to $500 deductible can slash your insurance costs by 20% or more. Go to $1000 and you save a lot of money. But you must pay the deductible if you need to make a claim !

- Multiple Insurances

I guess this might come under the ‘Get Multiple Quotes’ heading, but it’s still worth mentioning separately. You usually get an insurance break if you buy multiple policies with the same insurer.

This might mean multiple vehicles, or homeowner and auto insurance. Either way it’s worth asking about multi-policy discounts.

- Low Mileage

More and more people work at home. No more commuting. Fewer business trips. Low mileage on your car. Maybe you do travel to work, but car pool ?

Either way, look for low mileage discounts.

- Good Driving Record

A good driving record always reduces your auto insurance costs. Keep a clean drivers license. Don’t speed, don’t drive dangerously, and you’ll save money (apart from other benefits !)

- Bonus Tip

Okay, I said ‘7 Ways…’, but here’s some extra tips. Fit anti-theft devices to your car. Go on an advanced driver training course. Use daytime running lights. If you’re a college student away from home, consider adding to parents policy.

This short article covers the things you must consider when shopping for auto insurance. Follow these tips and you’ll slash your auto insurance costs.

Tinggalkan Balasan