Auto insurance is one of those things most people know they need, yet few truly understand. For many drivers, buying auto insurance feels like checking a box—find a policy, pay the premium, and hope you never need to use it. Unfortunately, this mindset often leads to overpaying, underinsuring, or missing opportunities to save money and improve coverage.

In today’s fast-changing economic environment, auto insurance has become more complex than ever. Rates fluctuate, policies change, and insurers continuously adjust how they calculate risk. The good news is that you are not powerless. With the right knowledge and strategy, you can take control of your auto insurance decisions.

This article breaks down seven essential auto insurance tips that every driver should understand. Whether you’re a first-time car owner or a seasoned executive managing multiple vehicles, these tips will help you save money, avoid common mistakes, and ensure your coverage actually works when you need it most.

Tip #1: Understand What You’re Really Paying For

Insurance Is Not One Product

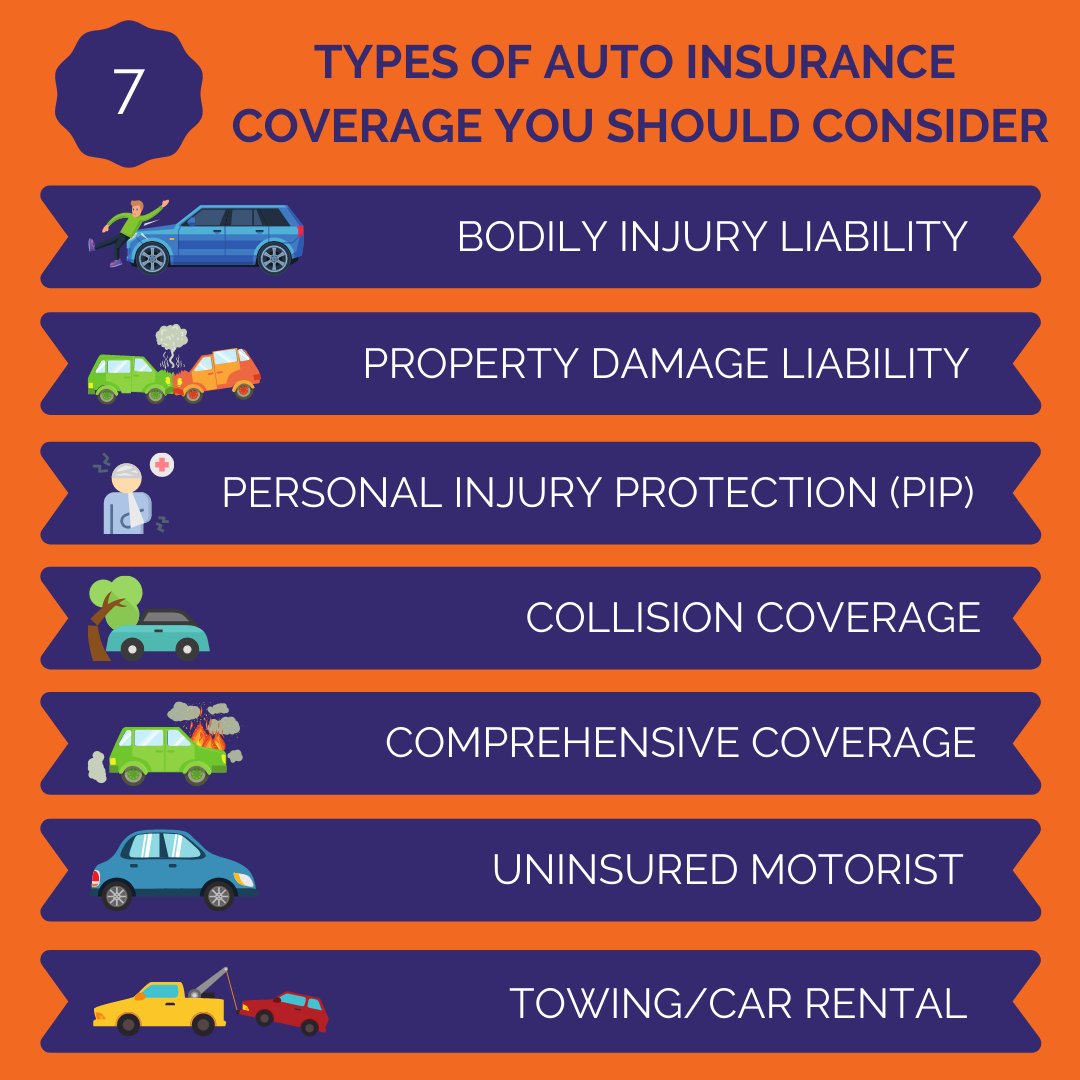

One of the biggest mistakes drivers make is assuming auto insurance is a single, simple product. In reality, it is a bundle of different coverages, each serving a specific purpose:

- Liability Coverage – Pays for injuries or property damage you cause to others

- Collision Coverage – Covers damage to your own vehicle after an accident

- Comprehensive Coverage – Protects against theft, vandalism, fire, and natural disasters

- Personal Injury Protection (PIP) – Covers medical expenses regardless of fault

- Uninsured/Underinsured Motorist Coverage – Protects you if the other driver lacks insurance

When you receive a quote, you are paying for a custom combination of these elements.

Why This Matters

Many drivers overpay because they don’t know which coverages they actually need. Others underinsure because they cut costs blindly without understanding the risks.

Understanding each component allows you to:

- Eliminate unnecessary coverage

- Increase protection where it truly matters

- Make smarter comparisons between insurers

Action Step

Ask your insurer for a line-by-line explanation of your policy. If they can’t explain it clearly, that’s a red flag.

Tip #2: Don’t Automatically Choose the Cheapest Quote

Cheap Insurance Can Be Expensive Later

A low premium looks attractive, especially when budgets are tight. But the cheapest policy often comes with:

- High deductibles

- Limited coverage

- Strict exclusions

- Poor claims service

When an accident happens, cheap insurance can quickly become very expensive.

What to Look Beyond Price

When comparing quotes, evaluate:

- Coverage limits

- Deductible amounts

- Claim settlement reputation

- Customer reviews and complaint records

Real-World Example

Two drivers pay different premiums:

- Driver A pays $80/month with low limits and a $1,500 deductible

- Driver B pays $105/month with better coverage and a $500 deductible

After an accident, Driver A pays thousands out-of-pocket, while Driver B pays very little. The cheaper policy ended up costing far more.

Action Step

Always compare value, not just price.

Tip #3: Use Deductibles Strategically

What a Deductible Really Does

Your deductible is the amount you agree to pay before insurance coverage kicks in. Higher deductibles mean:

- Lower monthly premiums

- Higher out-of-pocket costs during claims

The Smart Deductible Strategy

Instead of choosing the lowest deductible by default:

- Calculate how much you could realistically afford in an emergency

- Choose a deductible that balances savings and risk

Many drivers save hundreds per year by increasing deductibles slightly—without significantly increasing financial risk.

Executive Insight

High-income professionals often benefit from higher deductibles because:

- They have emergency savings

- They file fewer claims

- They focus on catastrophic protection rather than minor repairs

Action Step

Review your emergency fund, then adjust your deductible accordingly.

Tip #4: Take Advantage of Discounts Most People Miss

Discounts Are Often Hidden

Insurance companies rarely apply every available discount automatically. Many discounts require you to ask for them.

Common overlooked discounts include:

- Safe driver discounts

- Defensive driving course discounts

- Low-mileage discounts

- Multi-car discounts

- Bundling discounts (auto + home/renters)

- Vehicle safety feature discounts

Why Insurers Don’t Volunteer Discounts

Discounts reduce profit. Some insurers rely on customer inertia, assuming you won’t ask.

How to Unlock Savings

- Call your insurer annually and ask for a full discount review

- Update your profile when your driving habits change

- Provide proof of courses, safety features, or mileage reductions

Action Step

Make “discount review” a yearly habit.

Tip #5: Your Credit Score May Affect Your Premium

The Credit–Insurance Connection

In many regions, insurers use credit-based insurance scores to estimate risk. Statistically, drivers with better credit:

- File fewer claims

- Have lower claim costs

As a result, poor credit can mean higher premiums—even with a clean driving record.

What This Means for You

Improving your credit score can:

- Lower auto insurance premiums

- Unlock better coverage options

- Reduce overall financial stress

How to Improve Insurance-Related Credit Impact

- Pay bills on time

- Reduce outstanding debt

- Check credit reports for errors

- Avoid frequent credit applications

Action Step

Treat credit health as part of your insurance strategy, not a separate issue.

Tip #6: Review Your Policy Every Year (Not Every Decade)

Life Changes—Insurance Should Too

Your auto insurance needs change over time:

- New car purchase

- Job change or remote work

- Marriage or family growth

- Improved driving record

Yet many drivers keep the same policy for years without review.

Why Annual Reviews Matter

- Rates may drop due to improved risk profile

- Coverage needs may decrease

- New discounts may apply

- Better insurers may enter the market

CEO-Level Habit

Successful executives review contracts annually. Auto insurance should be no different.

Action Step

Set a calendar reminder to review your policy once per year.

Tip #7: Claims Strategy Matters More Than You Think

Not Every Claim Is Worth Filing

Filing small claims can:

- Increase premiums

- Remove claim-free discounts

- Label you as a higher-risk driver

Sometimes, paying minor repairs out-of-pocket is smarter long-term.

Smart Claim Decisions

Before filing a claim, consider:

- Repair cost vs deductible

- Impact on future premiums

- Frequency of past claims

Long-Term Thinking

Auto insurance is designed for financial protection, not convenience. Using it strategically keeps premiums lower over time.

Action Step

Reserve claims for significant losses, not minor inconveniences.

Bonus Tips for Smarter Auto Insurance Management

- Keep documentation of repairs and maintenance

- Use telematics programs if you are a safe driver

- Avoid coverage gaps at all costs

- Choose vehicles with good safety ratings

- Maintain a clean driving record consistently

Case Study: How One Driver Cut Premiums by 35%

Mark, a mid-level executive, applied these seven tips:

- Reviewed coverage and removed unnecessary add-ons

- Increased deductibles moderately

- Bundled auto and home insurance

- Improved credit score over 12 months

- Avoided filing minor claims

Result: 35% lower premiums over two years, with better coverage than before.

Conclusion

Auto insurance doesn’t have to be confusing, expensive, or frustrating. The key is shifting from passive buyer to informed decision-maker.

The 7 Auto Insurance Tips Recap:

- Understand what you’re paying for

- Don’t chase the cheapest quote blindly

- Use deductibles strategically

- Maximize available discounts

- Improve and monitor your credit score

- Review your policy annually

- File claims wisely

When you treat auto insurance as a financial tool rather than a mandatory bill, you gain control, confidence, and long-term savings.

Summary:

1> Raising your deductible

Deductible is the amount you pay from your pocket before making an insurance claim. The disadvantage of raising your claim is when you make a claim, you will pay more. However, if you are a safe driver, you will overtime save more money by raising your insurance deductible. Look at your previous insurance claim history and make a discreet decision for yourself.

2> Older Auto – Drop comprehensive / collision coverage.

If your car is not worth mu…

Keywords:

insurance, insurance broker, insurance agent, insurance tips

Article Body:

1> Raising your deductible

Deductible is the amount you pay from your pocket before making an insurance claim. The disadvantage of raising your claim is when you make a claim, you will pay more. However, if you are a safe driver, you will overtime save more money by raising your insurance deductible. Look at your previous insurance claim history and make a discreet decision for yourself.

2> Older Auto – Drop comprehensive / collision coverage.

If your car is not worth much, why pay for comprehensive and collision insurance coverage. You can visit a myriad of online sites to find true worth of your car. Additionally your insurance broker might be able to pull up the true worth of your vehicle.

3> Taking advantage of low mileage

Some auto insurance companies will give discounts if you drive less than a certain number of miles or drive less than a certain distance to work.

4> Moving – Consider insurance costs.

If you are considering moving, it will be a good idea to call your insurance agent and get his opinion on the insurance costs in the new city or state.

5> Low profile vehicle

Your vehicle will also determine your overall insurance costs. Some of the cars are favorite for thieves since they fetch a good price. Some cars are more expensive to repair. It makes a lot of sense to do adequate amount of research before you make your auto purchase.

6> Make sure your vehicle is correctly listed by your insurance agent.

Many manufacturers offer somewhat similar model names for vehicles but insurance costs may vary. Additionally 2 or 4 door or the wrong model can impact your auto insurance quote.

7> Have your insurance broker check other insurance company discounts.

A lot of companies will offer discounts if you and your spouse are insured with the same insurance company. Additionally, if you seek home insurance, life insurance, auto insurance from the same insurance company, you will get some discounts. Check with your insurance agent on saving money.

Tinggalkan Balasan